Dear Friends,

On behalf of all of us at BGSA Holdings and Cambridge Capital, we wanted to share some highlights of BGSA Supply Chain 2022. For those of you who joined us, we hope you had a great time.

This was a unique experience. For our 16th annual Supply Chain conference, we overcame the obstacles of COVID-19 and returned to our first in-person meeting since 2 years ago. Together, we were able to join with over 300 CEOs and leaders across all areas of the supply chain sector.

A Representative List of Industry Speakers and Leaders

For those of you who were not able to attend this year, we wanted to summarize what you missed.

2021 was the year the world discovered the importance of the supply chain. Some recent headlines illustrate this point:

- “The World Is Still Short of Everything. Get Used to It.” – New York Times

- “Big business bosses are warning that supply chain issues and inflation are here to stay” – CNBC

- “How a perfect storm of factors led to ‘the mother of all supply chain disruptions’” – Penn Today

- “Economists see supply constraints, labor shortages as bigger risks to economy than Covid-19” – Wall Street Journal

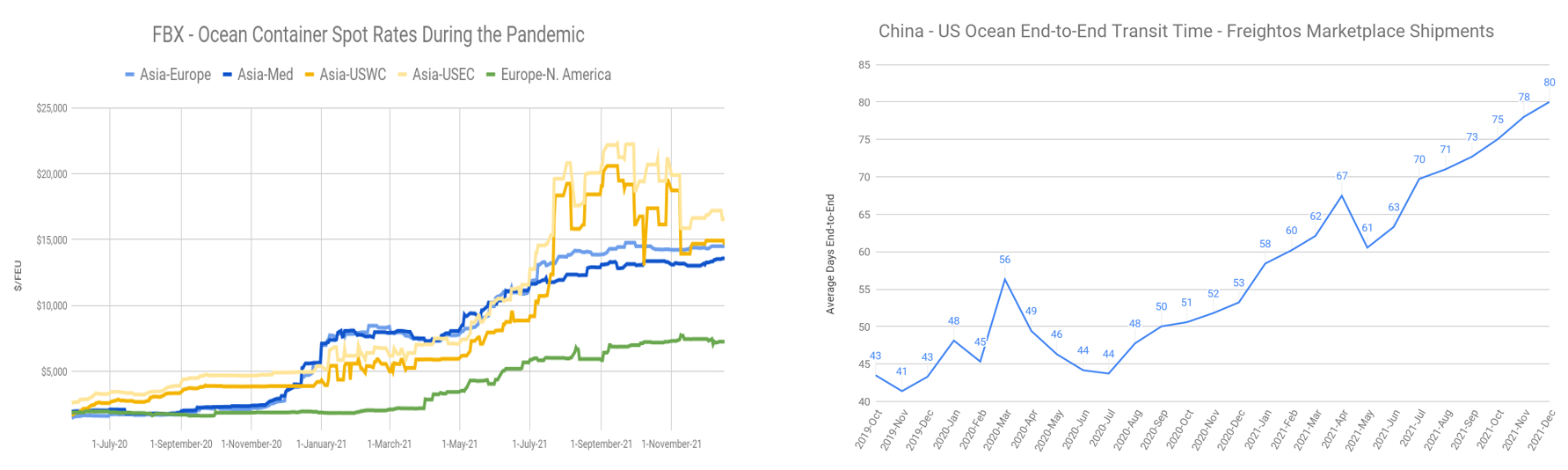

And from the outside, it appeared that the supply chain was broken. Ocean rates shot up from $3,000 to $20,000 per FEU. And congested ports drove delays, as China-US end-to-end transit time doubled from 40 to 80 days.

Table 1: Spiraling Ocean Rates, and Expanding Transit Times

Source: Flexport

Source: Flexport

In turn, shortages rippled through the economy. For instance, five of Ford’s top ten car models faced major delays. And GM’s CEO said the semiconductor shortage could cost GM $2 billion in lost earnings.

Given these challenges, you might expect supply chain companies to falter. Instead, they had a record 2021. What explains this surprise?

Let’s take a look at the data.

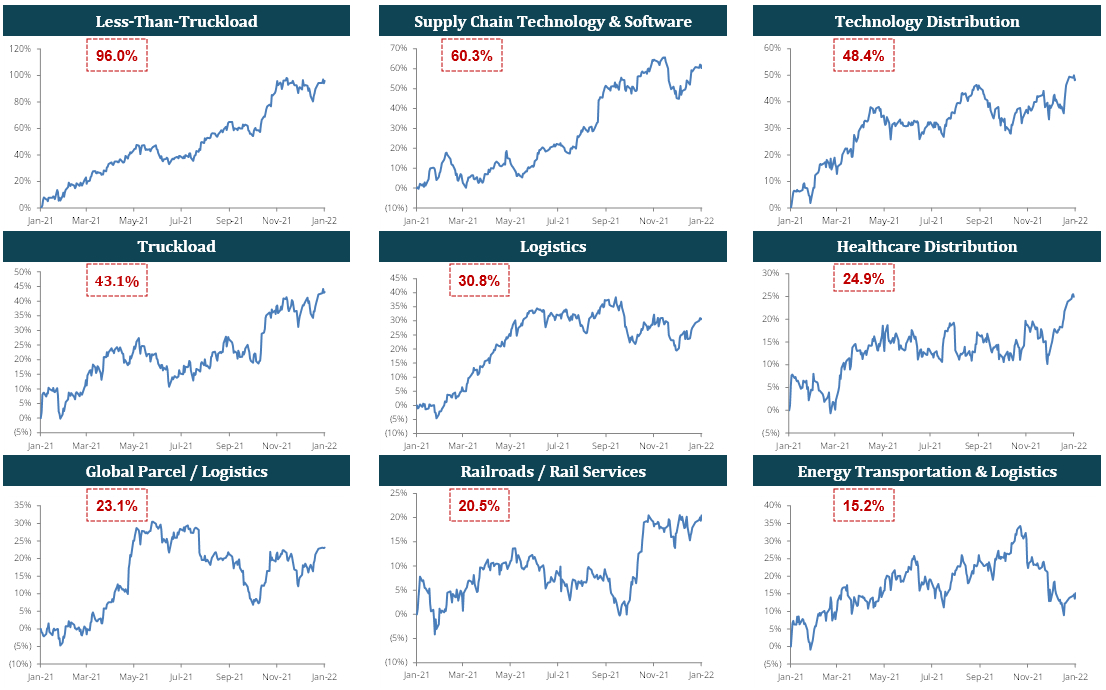

At BGSA, we track the BGSA Supply Chain Index, which is a basket of 60 companies across nine segments, including logistics, trucking, rail, supply chain technology, and all other related segments. In aggregate, the Supply Chain Index increased 28% in 2021. In addition, all nine segments produced a positive return.

The 2021 BGSA Supply Chain Index: Surge Led by LTL Software, Tech Distribution and Truckload

Source: Capital IQ, as of December 31, 2021

So how do we explain the fact that supply chain challenges have never been more evident, and yet supply chain companies are performing so well?

In sum, we see four key issues:

- Capacity crunch and low-cost networks

- Volatility surge

- eCommerce

- Innovation

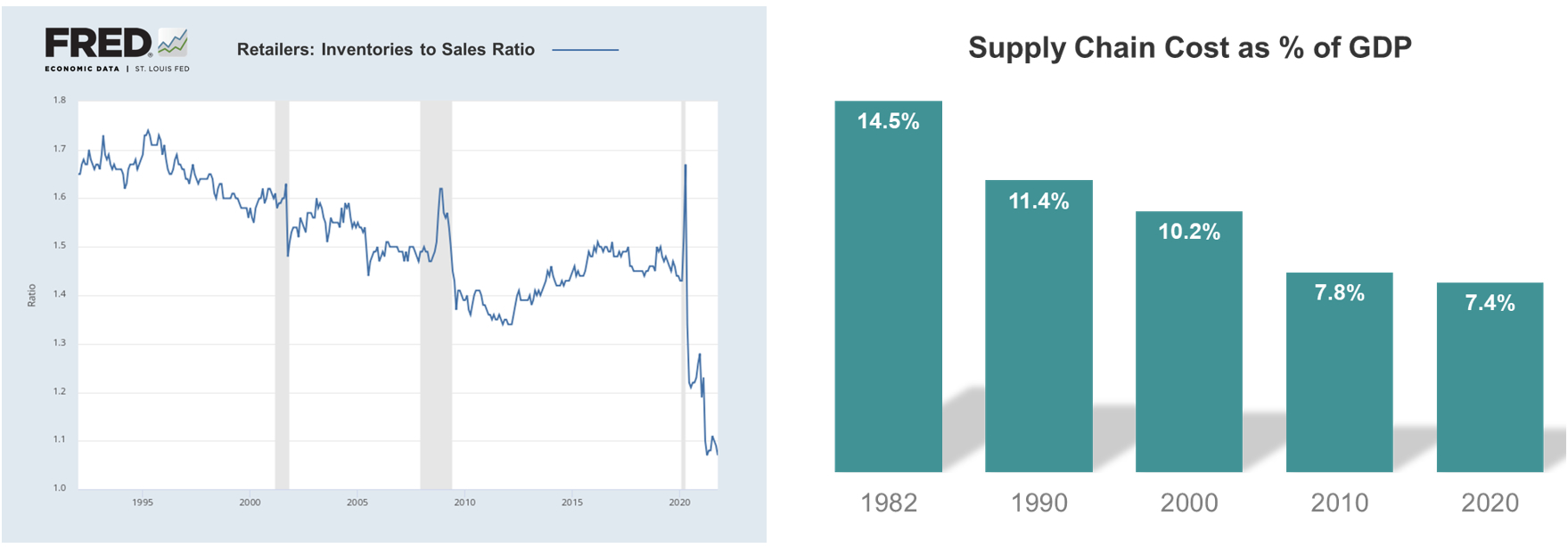

First, we are in midst of a record shortage of capacity. The last 30 years reflect a steady decline in inventory-to-sales. As the FRED government data illustrates, inventory to sales is now at an all-time low. This is a function of the rise of “just-in-time” supply chain strategies. As companies have run on an increasingly lean basis, they have chopped out excess inventory.

This lean strategy saved the US consumer a tremendous amount of money. 40 years ago, supply chain expenses represented 15% of GDP. Today, that expense is just 7.4%. The savings all accrued to the consumer. But that benefit came with a risk: shortages. We are now confronting that challenge.

Table 2: Record-Low Inventory Levels, and Supply Chain Cost Savings

As capacity has tightened, asset-based companies have benefited.

The data reflects this thesis. Less-than-truckload companies as a category shot up 96% in value. Indeed, 3 of the 5 publicly-traded LTL carriers spiked over 100%, including Yellow (up 186%), ArcBest (up 178%), and TFI (up 119%). The number one overall performer was truckload carrier PAM, which grew 204%. And logistics companies with asset-based networks, like XPO Logistics, continued to surge as well. XPO added $11 billion, growing its enterprise value from $15 billion to $26 billion.

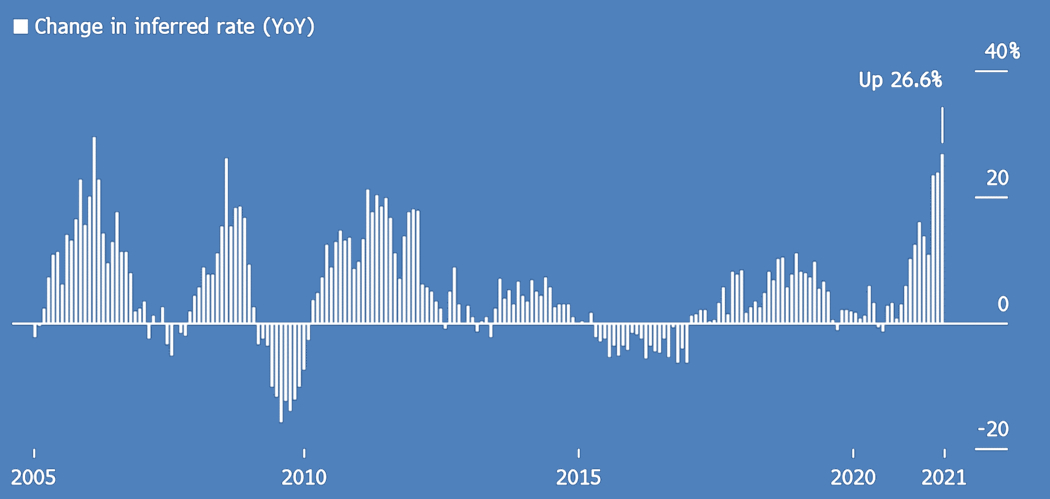

Second, we are witnessing a massive increase in supply chain volatility. From 2010 through 2020, freight rates consistently stayed within a fairly narrow range, typically not changing more than 10% per year. In 2021, we saw rates shoot upward rapidly and violently, reaching nearly 27%. These cost shocks rippled through the supply chain, delivering record profits to asset-based carriers while fueling 6.8% inflation.

Table 3: Supply Chain Volatility: Freight Rates in August Accelerated at the Fastest Level in 15 Years

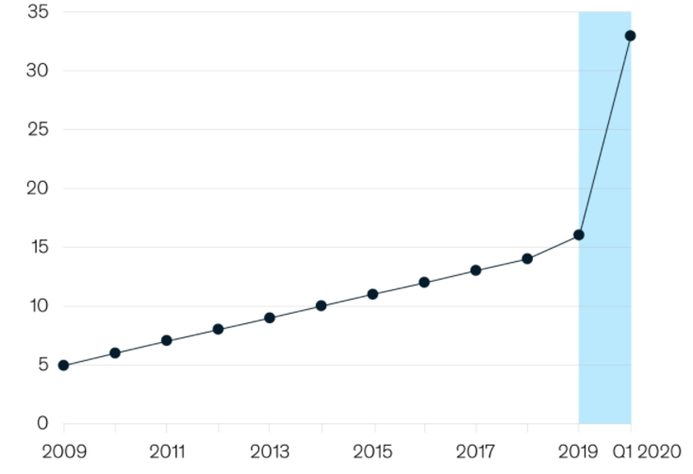

Third, ecommerce growth is driving new logistics needs. Consumer behavior has shifted suddenly. As McKinsey and others have noted, COVID compressed 10 years of forecasted ecommerce penetration into 3 months. As a result, supply chains must adapt. The ecommerce boom has caused a surge in last-mile software, in-market real estate, reverse logistics, and supply chain visibility, among other key areas.

Table 4: Ecommerce Penetration as a Percentage of Retail Shot up from 15% to Nearly 35%

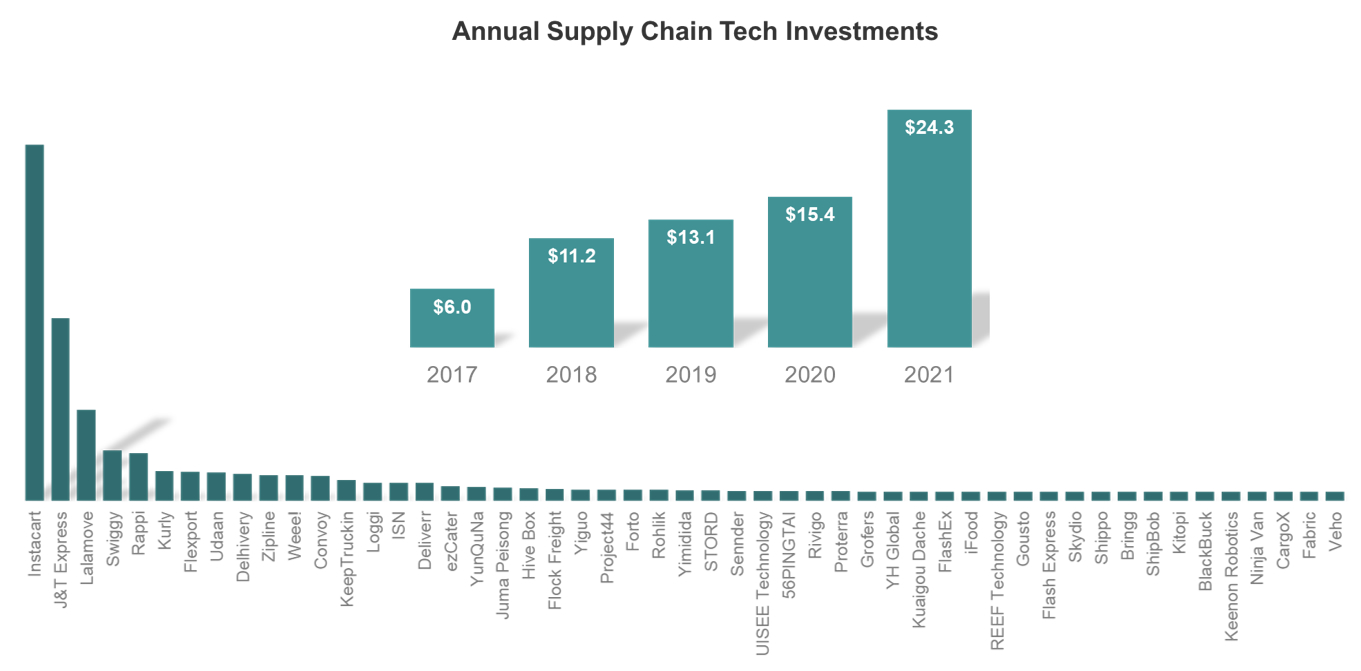

Fourth, the convergence of supply chain disruption and ecommerce growth has fueled a wave of innovation. Money is pouring into the supply chain sector. In the last 5 years, supply chain technology investment has shot up 4x, from $6 billion to $24 billion. And in the last year, the number of supply chain unicorns more than doubled, from 25 to 51!

Table 5: Supply Chain Technology Investment Quadrupled, Driving a More than 2x Increase in Unicorns this Year

Public market performance reflects this wave of software growth too. Supply chain software was the second-highest performing category in 2021, generating 60% growth. PFSweb and WiseTech increased 98% and 82%, respectively. And in the private markets, we saw even faster growth from many of the beneficiaries of the $24 billion of investment.

While investors were pouring capital into logistics, corporate acquirors stepped up their activity as well. In 2021, we saw record levels of M&A. These deals can be classified in five categories.

- Consolidators looked to buy up competitors. For instance, LaserShip bought OnTrac to build a denser regional network for next-day delivery.

- Ecommerce companies sought to move into logistics. Uber Freight acquired Transplace to combine transactional and contractual freight and data capabilities.

- Logistics companies pursued deals to expand in ecommerce. Maersk, fueled by a record profit of $17 billion, purchased Visible SCM to build a parcel logistics network.

- Infrastructure giants moved into services. The Port of Singapore Authority (PSA) bought BDP to create a global freight forwarding and logistics network. Meanwhile, DP World acquired Syncreon and Imperial Logistics.

- Retailers took control of their supply chain. In one of the most innovative moves of the year, American Eagle Outfitters bought Quiet Logistics and Airterra. Will other retailers follow suit?

Table 6: Supply Chain M&A Markets at Record Levels

Perspective at Cambridge Capital

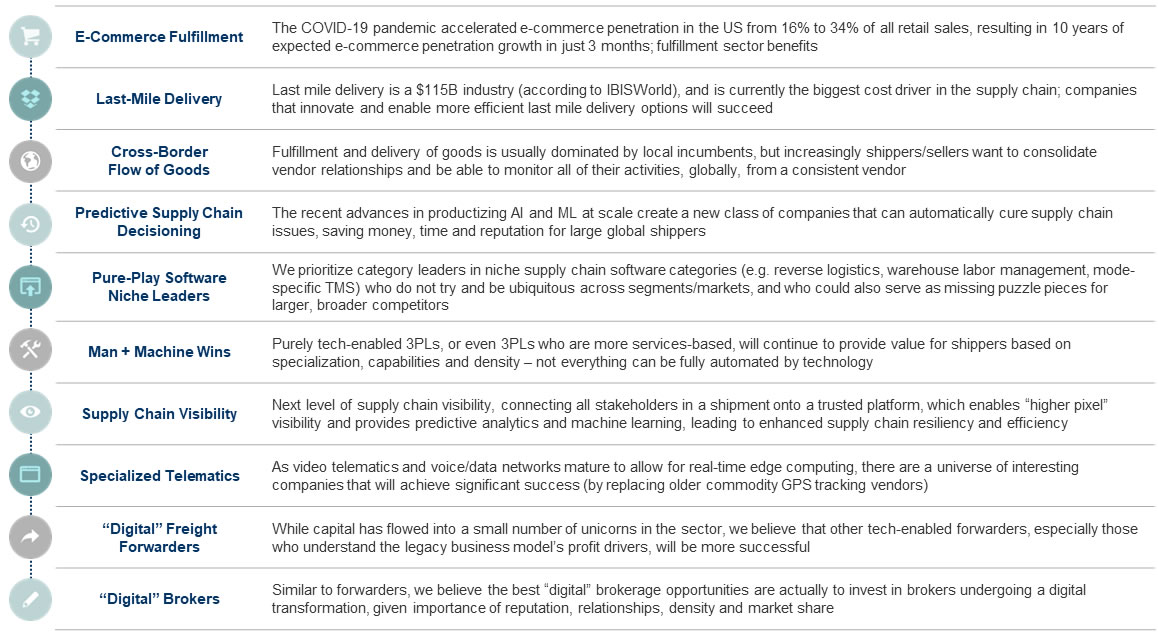

Our private equity firm, Cambridge Capital, specializes in the supply chain sector. At Cambridge Capital, we believe we are in the early innings of a transformation in high-growth digital supply chains. Some of the key themes we see include last-mile logistics, AI to automate supply chains, supply chain visibility, reverse logistics, and tech-enabled “man + machine” services. To illustrate these ideas, please see below.

Cambridge Capital Key Investment Themes

At Cambridge Capital, we believe in putting our money where our mouth is. We have made a series of investment in companies in these arenas. Here are four recent investments, along with the rationale:

- Bringg: for the B2C supply chain, last-mile delivery comprises 41% of total costs. In last-mile logistics SaaS, we believe Bringg is emerging as the market leader. We have backed them since 2016, have watched them scale up from a startup to the incumbent, and are pleased to welcome Insight Partners and others in backing one of the latest unicorns in logistics.

- ReverseLogix: as ecommerce increases, returns are shooting upward, since 30% of online purchases are returned. The reverse logistics market suffers from manual processes, a lack of visibility into returns data and metrics, and a poor customer experience. We believe ReverseLogix has built the first true end-to-end returns management system (RMS).

- Parcel Perform: ecommerce growth is also driving demand for supply chain visibility. Founded by DHL alumni, Parcel Perform understands the market gap in visibility, and is giving consumer brands and marketplaces a powerful tracking solution. We are proud to back them, along with Softbank.

- Everest: as freight markets continue to exhibit volatility, shippers need reliable and high-quality freight management companies. The Everest team has built a tech-enabled truck brokerage and logistics solution that is growing rapidly with blue-chip CPG companies.

We have a simple philosophy: back outstanding CEOs who are building top-quality businesses in all areas of the supply chain arena. Cambridge is willing to invest on a majority or minority basis, and focuses on $10-$50 million checks.

Cambridge Capital is currently seeking new investment opportunities, so please let us know if you would like to discuss how Cambridge may be a fit for your business. For more information, please feel free to contact me at Ben@CambridgeCapital.com.

Perspective at BGSA

On the advisory side, BGSA continues to expand its M&A services. BGSA has earned a reputation as a leader in M&A for transportation, logistics, and supply chain services, and has worked on over 50 transactions in the sector. Clients and transactions have included NFI, C.R. England, GENCO (now FedEx), New Breed (now XPO), and many others.

BGSA continues to play an active role as trusted advisor to major companies in the sector. Just this week, BGSA’s client Werner Enterprises announced the sale of Werner Global Logistics to Scan Global Logistics Group. Please reach out to BGSA if you’d like to discuss deal ideas.

If you would like to discuss acquisitions, divestitures, or other deal ideas, please reach out to Jon Taylor and Shai Greenwald, at Jon@BGSA.com and Shai@BGSA.com.

Closing Thoughts

In sum, we thank you for being a part of the BGSA Supply Chain ecosystem. We all learn and benefit from the collective wisdom of this outstanding network of CEOs and industry leaders.

To see highlights from 2022’s event, feel free to click here.

Please save the date for next year’s BGSA Supply Chain Conference: January 18-20, 2023. Next year we will again return to the Breakers in Palm Beach, for our 17th annual conference!

Meanwhile, we look forward to a successful 2022 for our clients, to a busy year of strategic advisory work with BGSA Holdings, and to a few more outstanding platform investments with Cambridge Capital. If you would like to discuss strategic, financial, or other ideas, please feel free to contact me directly at (561) 932-1601 or Ben@BGSA.com.

Thank you and best wishes for the coming year.

Sincerely,

Benjamin Gordon